IEA (2023), Electricity Market Report – Update 2023, IEA, Paris https://www.iea.org/reports/electricity-market-report-update-2023, Licence: CC BY 4.0

Executive summary

Falling electricity consumption in advanced economies weighs on global growth in power demand

Global electricity demand growth is expected to ease in 2023 before accelerating in 2024. Demand is expected to grow by slightly less than 2% in 2023, down from a rate of 2.3% in 2022 and the average annual growth rate of 2.4% observed over the 2015-2019 period. This moderation is strongly driven by declining electricity demand in advanced economies, which are dealing with the ongoing effects of the global energy crisis and slower economic growth. In 2024, as expectations for the economic outlook improve, global electricity demand growth is forecast to rebound to 3.3%.

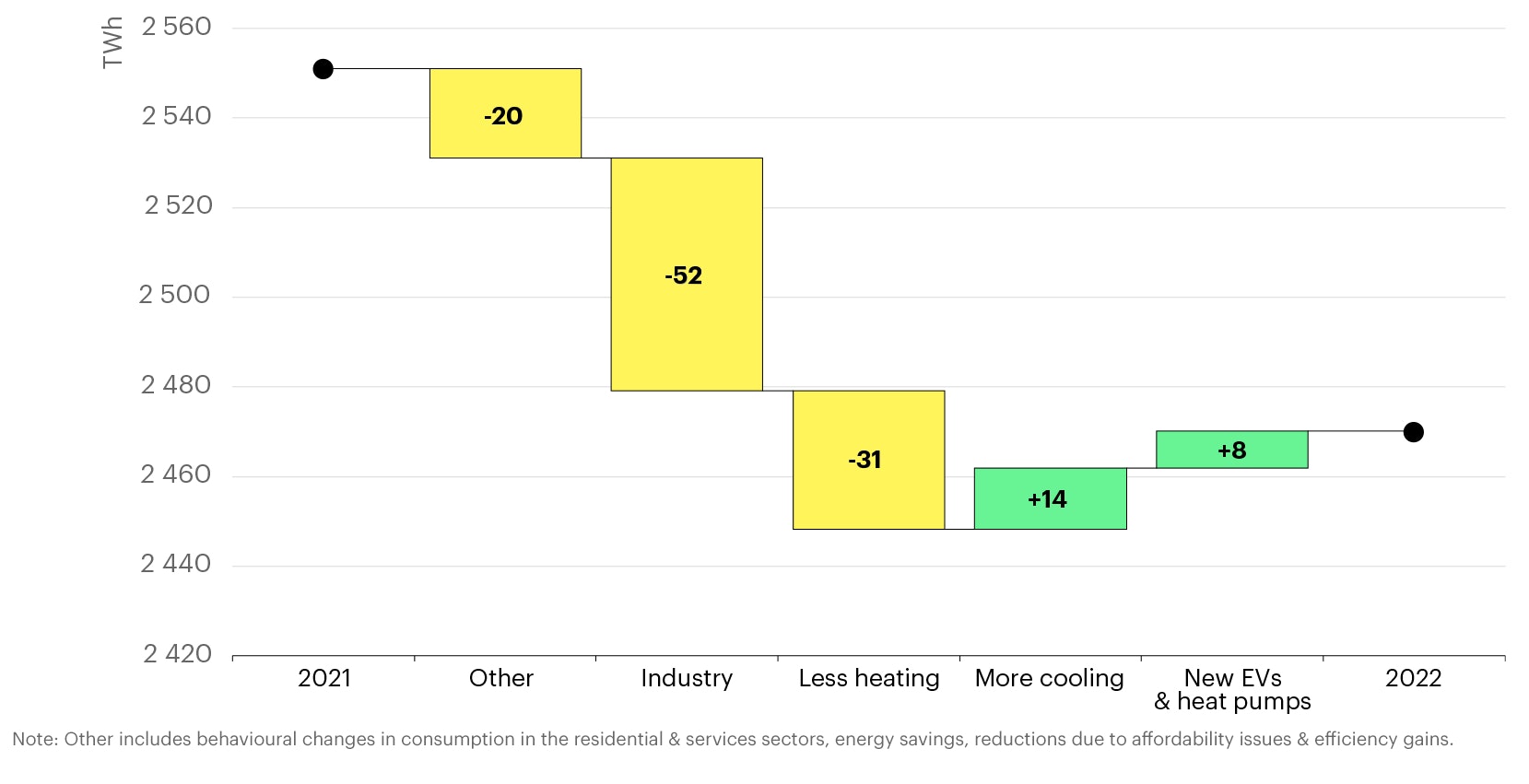

Electricity demand in the European Union is set to decline in 2023 for the second year in a row, falling to its lowest level in two decades. EU electricity demand is expected to record a 3% drop in 2023, after already falling 3% in 2022. This is despite strong growth in electrification with a record number of electric vehicles and heat pumps sold. Following these two consecutive declines, which together amount to the region’s largest slump in demand on record, EU electricity demand is set to drop to levels last seen in 2002.

Europe's energy-intensive industries have not yet recovered from last year’s production slump, as evidenced by the staggering 6% year-on-year decline in total EU electricity demand during the first half of 2023. Almost two-thirds of the net reduction in EU electricity demand in 2022 is estimated to be from energy-intensive industries grappling with elevated energy prices. This trend has continued well into 2023, despite the prices for energy commodities and electricity falling from their previous record highs. As policy developments abroad courting industrial investment put pressure on Europe’s industrial competitiveness, the European Union is at a crossroads. The outcome of policy discussions now underway could determine the future of its energy-intensive industrial sector.

Estimated drivers of change in electricity demand in the European Union, 2022 vs. 2021

Open

{kind=link}

The substantial demand declines in advanced economies contrast sharply with the growth observed in emerging economies such as China and India. Japan is similarly expected to record a significant 3% fall in electricity demand in 2023, while the United States is set to see a decrease of almost 2%. In contrast, China's electricity demand is expected to increase by 5.3% in 2023 and 5.1% in 2024, slightly below its 2015-2019 average of 5.4%. India is set to have an average annual growth rate of 6.5% over the outlook period, surpassing its 2015-2019 average of 5.2%.

Declines in fossil-fired electricity generation are becoming structural

The accelerated pace of new renewable capacity additions shows that renewable generation could surpass coal as early as 2024, if weather conditions are favourable. This is supported by the expectation that coal-fired generation will slightly decline in 2023 and 2024 after rising 1.5% in 2022, when high gas prices boosted demand for alternatives. Increases in coal-fired generation in Asia in 2023 and 2024 are poised to be offset by strong drops in the United States and Europe.

Renewables are set to meet all additional demand in 2023 and 2024. With global demand growth easing in 2023, incremental increases in renewables alone are expected to cover all additional demand not only this year, but also in 2024, when demand growth is expected to accelerate again. By 2024, the share of renewable generation in global electricity supply will exceed one-third for the first time.

Year-on-year global change in electricity generation by source, 2019-2024

OpenBy 2024, electricity generation from fossil fuels is expected to have fallen four times in six years. Declines in fossil-fired generation were rare in the past and occurred primarily after global energy and financial shocks, such as following the oil crises of the 1970s or during the Great Recession in 2009, when overall electricity demand was suppressed. But in recent years, fossil-fired supply has lagged or fallen even when electricity demand expanded. These trends – driven by the strong growth in renewable generation – suggest the declines in fossil electricity generation are becoming structural. The world is rapidly moving towards a tipping point where global electricity generation from fossil fuels begins to decline and is increasingly replaced by electricity from clean energy sources.

Emissions from power generation are poised to dip slightly through 2024

Increases in emissions from power generation in China and India are expected to be more than offset by declines in other regions. The European Union alone accounts for 40% of the total decline in emissions from power generation expected to occur in 2023 and 2024, excluding China and India. The EU is followed by the United States, where renewables deployment is growing strongly, and gas is increasingly replacing coal-fired supply. Extreme weather, unexpected economic shocks and changes to government policies can cause an uptick in emissions in specific years. However, the overall trend of global power sector emissions plateauing is expected to persist, with years in which emissions decline, not rise, becoming more frequent.

Changes in global CO2 emissions from electricity generation, 2024 vs. 2022

OpenWholesale electricity prices signal increased need for flexibility

The number of hours in which electricity prices dropped below zero doubled in European countries such as Germany and Netherlands in the first half of 2023 compared to the same period in 2022. This was driven by strong renewables output at times of significantly reduced demand. Meanwhile, in other markets such as South Australia, which has a very high penetration of variable renewables, the trend was even starker. Prices on the wholesale electricity market there fell below zero almost 20% of the time in 2022, compared to less than 1% of the time in Germany and the Netherlands. Negative prices indicate generation is not sufficiently flexible, the demand side is not adequately price-responsive or there is not enough storage to conduct energy arbitrage. Negative prices also provide signals to invest in solutions and technologies to improve system flexibility. These signals will have to be accompanied by updated regulatory frameworks to incentivise demand-side flexibility and storage in order to increase the flexibility of the broader system.

Wholesale electricity prices remain elevated in many countries despite substantial declines, although there are regional differences. As prices for energy commodities such as gas and coal have fallen significantly in the first half of 2023, wholesale electricity prices in many regions have declined from their previous peaks. European wholesale prices halved from their record highs in 2022, falling closer to their 2021 average. Despite this, average prices in Europe are still more than double 2019 levels. Similarly, average wholesale electricity prices in India in the first half of 2023 were still 80% higher than 2019 levels, and in Japan they were 30% higher compared to 2019. In contrast, wholesale electricity prices in the United States have almost fallen back to 2019 levels.

Quarterly average wholesale prices for selected regions, 2019-2024

OpenImpact of weather on electricity demand and supply is increasingly noticeable

Rising demand for cooling is straining the world’s power systems. Summers with extreme temperatures are becoming more frequent in many regions, elevating electricity demand for cooling systems and stretching power supplies. As more households start purchasing air conditioners, the impact will increase in many countries – especially in emerging economies that currently have a much lower share of households with AC than advanced economies with comparable climates. Setting higher efficiency standards for air conditioning would greatly help limit the impact of additional cooling demand on power systems. To ensure system reliability, it will be crucial to have adequate backup generation capacities, encourage demand management and energy storage, accelerate grid investments, and enhance fuel supply security for power plants. Insufficient preparedness in these areas could lead to more frequent stress on grids, resulting in load-shedding and blackouts.

The availability of hydropower requires greater attention. The capacity factor of global hydropower has been in decline over the past decade, falling from an average of 38% in 1990-2016 to about 36% in 2020-2022. This difference of two percentage points means that, globally, today’s hydropower capacity is producing about 240 TWh less electricity per year than would have been the case if capacity factors had remained unchanged. This indicates a volume of energy as large as Spain’s annual electricity consumption needs to be supplied instead by other sources, a gap that is currently filled mostly by fossil-fired generation. Recent years saw intense droughts that caused a significant reduction in hydropower availability in affected regions such as Europe, Brazil and China. Anticipating challenges on hydropower related to climate change, and planning accordingly, will be crucial for the efficient and sustainable use of hydro resources.